IRS Form 843 Claim for Refund and Request for Abatement, is an important tool for taxpayers seeking relief from certain IRS penalties, interest, and specific taxes. While it’s not the…

If you have unpaid taxes, the IRS may have already taken or may soon take collection action against you, such as filing a lien, issuing a levy, or rejecting an…

If you owe taxes to the IRS, you may find that your ability to travel outside the U.S. is restricted. Once the IRS determines your tax debt to be seriously…

Failing to file your tax returns may seem like something you can deal with later, but the longer you wait, the more serious the consequences become. Whether it’s one year…

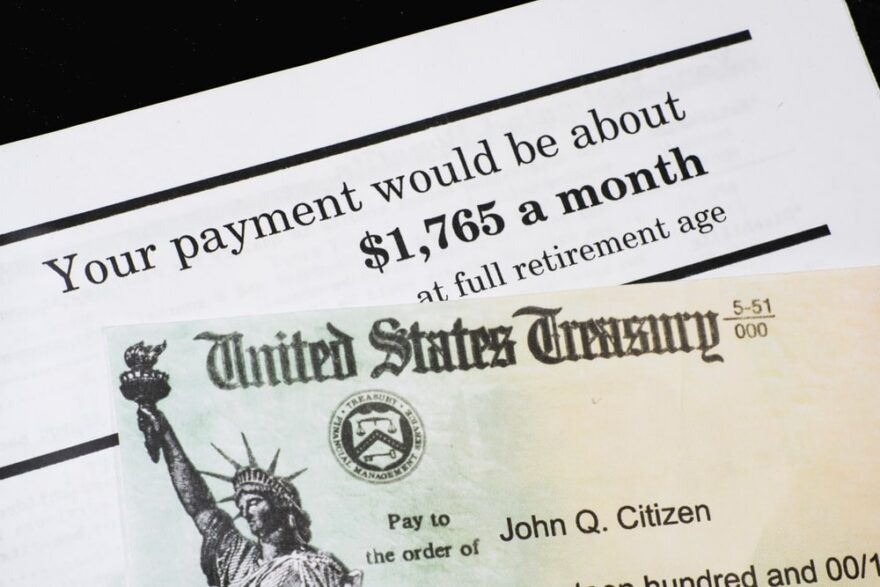

Owing back taxes to the Internal Revenue Service can be quite stressful. This situation can become even more overwhelming for individuals who rely on Social Security benefits as their primary…

In 2024, you may have made substantial gifts to your children, grandchildren, or other family members as part of your estate planning. Or maybe you just wanted to help those…

There are many reasons why taxpayers have IRS tax problems, and on rare occasions, it is due to criminal intent. However, most tax problem resolution cases we deal with are…

You're not alone if you're facing tax debt issues in Boca Raton. Many individuals and businesses struggle with IRS notices, back taxes, penalties, and interest that can quickly spiral out…

If you’ve ever dealt with IRS collections, you know how frustrating, exhausting, and sometimes infuriating the process can be. Between confusing notices, long wait times, and aggressive collection tactics, the…

”East Coast Tax Consulting Group helped to resolve my issues with the IRS. I was able to save thousands of dollars and put my IRS tax problems behind me once and for all.

B.K.Boynton Beach

”My wages were going to be levied and I called East Coast Tax for help. They worked quickly to have the levy released and set-up a payment plan for me with the IRS. I found them to be knowledgeable and friendly.

J.W.Boca Raton

”East Coast Tax Consulting handled the audit of my tax returns and resolved the matter without me having to pay any additional tax. They are very knowledgeable and were quick to respond to my questions. I highly recommend them.